Did you miss me? The company I work for has gone through a transition (more to come on that at a later date) and there were some regulatory hurdles I had to cross before I could send this update again. I am still open for business.

Interest Rates

Since Patrick Reed won the Masters home loan rates have worsened. In fact, mortgage rates are presently at the highest levels in over four years.

A look at the chart for the US 10-year treasury yield shows that we have to go back to January of 2014 to find a time when interest rates were as high as they currently are.

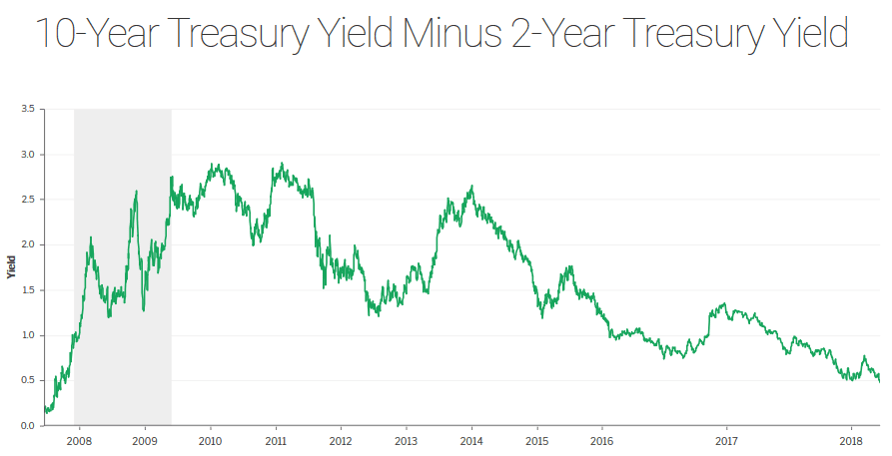

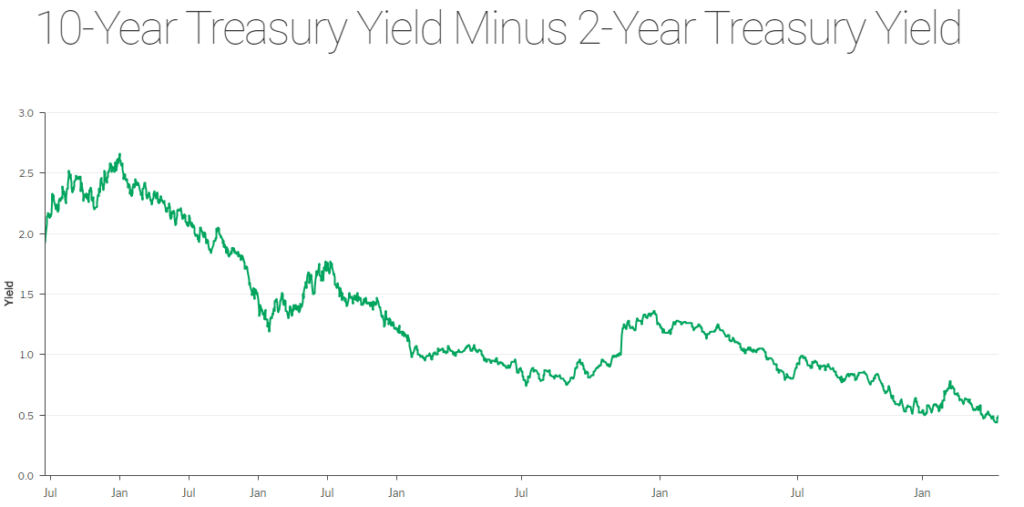

Yield Curve Flattening

Longer term interest rates are not the only section of the yield curve that are rising. If you have a Home Equity Line of Credit or balance outstanding on a credit card then you also know rates have been rising on the short-end of the yield curve. In fact, the short-end of the yield curve is rising faster which is why the yield curve is flattening.

Dating back to 1975 everytime the yield curve has completely flattened a recession has occurred. Given the economy seems to be chugging along nicely I don’t believe we’ll see a recession in the near-term. Therefore, I think the longer end of the yield curve will rise. Translation: I believe mortgage rates are poised to increase as the year goes on.

The Week Ahead

There are a lot of significant economic reports due out this week that can influence the direction of mortgage rates.

Earlier today the National Association of Realtors reported that existing home sales were stronger than expected. A lack of inventory continues to be a challenge in the housing market and therefore median home prices continue to rise.

We will learn more about home prices rising on Tuesday when the latest Case-Shiller home price index is reported. Also on Tuesday is consumer confidence and new home sales.

At the tail end of the week we’ll get readings on durable goods, gross domestic product, and the employment cost index.

Current Outlook: locking bias