Tag: mortgage rates

Will the US recession in 2024 affect home prices in Portland?

Will there be a recession in 2024? What does that mean for home prices in the Portland area? Watch this video to learn more!

Fitch Announcement!

How is the US credit rating announcement impacting mortgage rates?

Watch to learn more!

US Debt Limit’s impact on mortgage rates

A special video Rate Update

Given the extraordinary circumstances we are currently experiencing I have prepared a special video ‘rate update’ for today.

Please take 4 minutes to watch this special message below:

Current Outlook: Floating

Mortgage rates at all time lows. Might they go even lower?

Home Loan Rates

Mortgage rates are presently at all-time lows which were originally established in 2012 and again in 2016. Could home loan rates go even lower?

The Coronavirus

Although new cases of the Coronavirus are slowing in China the number of people infected in other countries is growing. Furthermore, there is fear that some countries are underreporting the true number of citizens infected with the virus.

Fear over the spread of the illness is now having a significant impact on financial markets around the globe.

Impact on Financial Markets

On Monday US & European stock markets fell by ~3% and today they are off over 1%. Japan’s stock market fell 3.3% on Monday.

When stocks decline it tends to drive capital into the bond market which pushes interest rates lower. The US 10-year treasury note is now trading at 1.322%, an all-time low) and the yield curve is now inverted.

An article published by Bloomberg reported that unless economic activity resumes 66% of small to medium sized businesses inside China are poised to run out of cash within two months.

Home Prices

According to the S&P CoreLogic Case-Shiller Home Price Index appreciation picked up nationwide at the end of 2019. The report showed that homes increased by 3.8% during 2019.

With interest rates hitting all-time lows I expect home price appreciation will remain healthy for the foreseeable future.

The week ahead

There is plenty of significant economic data being reported this week. Specifically, I will be paying attention to New Home Sales (Wednesday), Gross Domestic Product (Thursday), Pending Home Sales (Thursday), and Personal Income (Friday).

However, news regarding the Coronavirus is the primary driver of interest rates at this moment. If it appears that the illness continues to spread then I expect stocks to continue to falter and mortgage rates to improve further.

Current Outlook: Floating

Mortgage rates enter new range

Although it is illegal to sell a body part in the United States thousands of people do it every day. On this day in 1881 the American Red Cross was founded. Since then people have been selling pints of blood for a cup of juice and a cookie nearly every day.

Mortgage Rates

Mortgage rates worsened modestly last week. The US 10-year treasury note, which home loan rates tend to track, is now yielding over 3.00%. It is at the highest level since 2011.

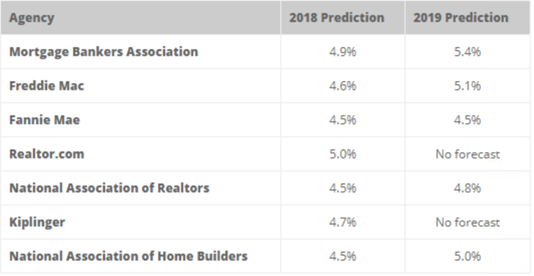

Most every analyst’s interest rate prediction for 2018 has been surpassed including my own. I thought mortgage rates would increase to 4.625%-4.875%. Here is what others thought:

US Stocks

The Dow Jones Industrial Average reacted positively to comments made by US Treasury secretary Steve Mnuchin earlier today. He stated that the trade dispute between the US And China was “on hold”. The Dow spiked 350 points at the opening bell.

When stocks rally it tends to hurt mortgage rates.

The Week Ahead

This week’s economic calendar is fairly light. On Wednesday we’ll get minutes from the May 2nd Fed meeting which can always move the markets. Aside from that I’ll be watching New Home Sales (Wednesday), Existing Home Sales (Thursday), and the FHFA Home Price Index (Thursday).

Outlook

It appears that rates have entered into a new trading range. I expect the current level of rates to be at the lower end of the range with room for them to be .25% higher than current levels. I recommend locking.

Current Outlook: locking

Rates end Q1 on a positive note but higher rates likely later in the year

At the end of her life my wife has already decided to be buried at the golf course so that I visit her multiple times per week. It’s’ Masters week which means my productivity at work will decline significantly starting Thursday.

Quarterly Report

Interest rates had a tough start to the year increasing by approximately .50% during the first seven weeks. Peaking on February 21st mortgage rates have since flattened and even improved modestly.

For the quarter mortgage rates increased by about .375%.

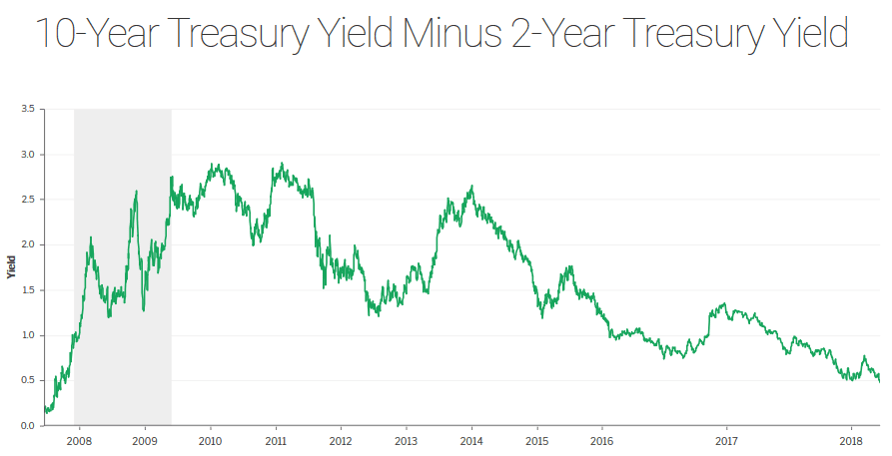

Yield Curve

The yield curve is at the flattest point since 2007. The yield curve measures interest rates over a variety of durations. The chart below depicts the difference between the yield on the 2-year and 10-year treasury notes. As the difference declines the yield curve gets flatter.

A flat yield curve is thought to forecast either an economic slowdown or higher long-term interest rates in the future. Given that the economy appears to be stable I think we are in for higher mortgage rates later in the year.

US Stocks

Home loan rates are currently benefiting from volatility in the US stock market. Equities are off ~2% again today as investors fret over the possibility of trade wars with China and regulatory backlash on tech companies. When stocks do poorly interest rates tend to benefit.

The Week Ahead

It’s the first week of a new month so we’ll get the all-important jobs report this Friday. Analysts are most interested in average hourly earnings which has remained sluggish despite low unemployment. A higher reading for hourly earnings would be unfriendly to mortgage rates. The remainder of the economic calendar is light.

Mortgage rates are presently at the lower end of their recent range so I will recommend locking.

Current Outlook: locking

Stocks slide and mortgage rates hang steady

If you’re like me then your NCAA men’s basketball bracket is officially busted. With two #1 seeds eliminated in the first weekend I will now focus my sporting attention on the upcoming Masters golf tournament. Speaking of golf, do you know why Virginia and Xavier fans only plan 14 holes? They can’t make it to the final four.

US stocks slide

US stocks fell by approximately 1% last week and are down sharply again today on news that data from Facebook may have been breached in 2016 and improperly used by a third party vendor in the presidential election. Facebook shares are bringing down the broader market.

When stocks decline it typically helps interest rates improve. Thus far mortgage rates are basically unchanged.

The Fed

The Federal Reserve Open Market Committee is scheduled to meet Tuesday-Wednesday with a monetary policy statement slated for Wednesday. The markets fully expect the Fed to hike short-term interest rates by .25%. This is already baked into the mortgage rate offerings you see today.

What can cause interest rates to move are the comments that accompany the rate hike announcement. Will the Fed move more aggressively to hike rates in lieu of recent fiscal stimulus? Or given that recent inflation and wage growth data has been tepid will they stay the course with a “gradual” approach?

Don’t be alarmed when you hear Wednesday afternoon that the Fed is hiking rates by +.25%. It does not necessarily mean that mortgage rates will follow suit.

The rest of the week

Aside from the highly anticipated Fed meeting I will be watching for the FHFA home price index report due out on Thursday and durable goods along with new home sales on Friday.

From a technical standpoint the yield on the US 10-year treasury note remains below 2.91%. As long as this is the case rates should remain near current levels.

Current Outlook: floating

Home Loan Rates stable….for now

With today being the first Monday after daylight savings I think we can all agree this is the “Mondayest” Monday of the year.

Mortgage rates stable?

Mortgage rates fared ‘OK’ last week. For the most part home loan rates were unchanged despite US stock indexes moving higher. Normally interest rates worsen when stocks do well.

Don’t look now but mortgage rates have traded within a .125% range since mid-February.

Jobs report

Last Friday’s all-important jobs report showed much stronger employment growth than was expected. However, wage growth actually slowed modestly which is probably why mortgage rates didn’t move higher on the news. Higher wages can lead to inflation which is the nemesis of mortgage rates.

Rates getting squeezed

The technical outlook for interest rates has me concerned that we may experience a “breakout”. The yield on the US 10-year treasury note is trading in a tight range between technical support and resistance. When this happens we sometimes see yields sharply bounce outside of the compressed range.

The week ahead

This week’s economic calendar features a variety of reports that can drive interest rates. Later today the US Treasury will auction off $21 billion in US 10-year treasury notes. If demand weakens for this asset it would likely pressure home loan rates higher.

On Tuesday we’ll get the latest reading of the Consumer Price Index, on Wednesday Retail Sales, and on Thursday the Producer Price Index.

The safe play is to lock and avoid any possible breakout.

Current Outlook: locking bias