As you may be aware mortgage rates are on the rise which is negatively impacting home affordability.

Over the past five weeks average fixed rate home loan rates have increased by ~.50%. Many analysts think that rates will continue to rise for the remainder of the year.

How much does higher interest rates impact home affordability? Take a moment to watch the video below for an explanation.

A .50% increase to mortgage rates effectively translates to a +6.3% increase to home prices.

In other words, a +.50% increase to interest rates for a conventional 30-year fixed rate mortgage has the same impact on monthly payments as if interest rates were unchanged and homes were 6.3% more expensive.

If rates should increase by an additional .50% over the remainder of the year this would make homes ~12% more expensive even homes don’t appreciate as a result of the basic tenets of supply and demand.

Given that many analysts think both mortgage rates and home prices are expected to increase for the remainder of 2018 it may be significantly less affordable to buy a home in the future than it is today.

Are you curious to learn about the options you have to purchase a home today? Contact us for a no obligation review.

Congratulations to the Philadelphia Eagles who won their very first Super Bowl Championship yesterday. As for the Patriots, do you know the difference between a New England fan and a carp? Answer: One is a bottom-feeding, scum sucker, and the other is a fish.

Mortgage rates continue to march higher. I know this may seem repetitive but it’s not like we didn’t see this coming (see HERE, HERE, and HERE).

Supply & Demand

The basic concept of supply and demand can explain why we’re witnessing home loan rates rising. Rates are effectively determined by the price of mortgage-backed bonds (MBS’s). When the price of bonds fall then mortgage rates rise and vice versa.

The Federal Reserve

Starting in 2017 the Fed began to unwind the balance sheet which they accrued during the aftermath of the housing crash. The Fed had been investing billions of dollars per month into the fixed income market including MBS’s. In the absence of the Fed’s investment demand for MBS’s has declined pushing prices down and yields up.

European Central Bank

The US central bank was not the only entity dumping money into quantitative easing (QE) measures following the recession. The European Central Bank followed the US’s lead and became a major investor in the European fixed income market. They recently discontinued their QE and that has also drawn demand away from the US further pressuring prices down and yields up.

Higher deficits

Not only is demand for fixed income securities declining but the US government will be increasing the supply of US Treasury notes and bonds in the coming years in order to fund the recently passed tax cuts. Should congress and the president also sign an infrastructure bill into law we could expect to see higher deficits and a greater supply of fixed income securities competing with MBS’s.

The bottom line is that we are in an environment where the demand for MBS’s has declined and the supply of competing debt securities is increasing. As a result yields are rising.

I expect this trend to continue in the immediate term. I think mortgage rates will worsen by another .125%-.25% before stabilizing.

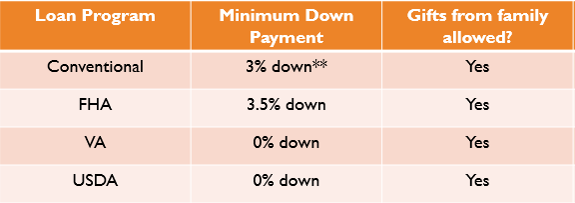

I came across an article over the weekend which stated that roughly 40% of US citizens between the ages of 25-34 believe that lenders require at least 15% down payment in order to purchase a home. This may be one reason why those in the “millennial” generation have lagged their predecessors in home-ownership rates (there are certainly other factors). The truth is that there are many programs which allow for less than 5% down and all of them allow the down payment to be 100% gifted by a family member.

Of course all these programs are subject to qualifying and there are some caveats. But, if you or someone you know has been putting off buying a home because they thought they needed to save more money its probably worth exploring options now given that interest rates are very attractive and most analysts believe home prices will continue to rise. I’d love to be a resource for you so don’t hesitate to let me know if you’d like to engage in a conversation about your circumstances.

On Tuesday President Trump will deliver the annual State of the Union Address to Congress. Some people think that Congress should work towards increasing the Federal minimum wage. If anyone knows about doing the minimum for their wage it seems like a great place to start.

What legislative priorities will the President focus on in his speech? Any emphasis on infrastructure spending could add fuel to the fire in terms of mortgage rates increasing.

The tax reform law which passed in December has already added $1.5 trillion in deficit spending over the next decade. Additional infrastructure investment without means to pay for it would put further pressure on interest rates to move higher (CLICK HERE to learn how).

Interest rates are currently at the highest levels since April of 2014. There are a variety of factors contributing to higher home loan rates.

Notably the Fed has been hiking short-term interest rates for the past couple years and the longer end of the yield curve has remained flat. It appears longer durations are following suit.

On Tuesday the latest S&P Corelogic Case-Shiller Home Price Index will be released as well as Consumer Confidence.

This column has been recommending a locking position ever since the US 10-year treasury note eclipsed 2.50% back on January 10th. Since then mortgage rates have increased by .25%-.375%. I continue to recommend a locking stance.

Hi. I’m Evan Swanson, mortgage professional and certified financial planner based in Portland, Oregon.

Today I’m going to help answer a question we get frequently, which is how much house or how much mortgage can I afford?

What I’ve done is prepared a hypothetical scenario that we’re going to use to help answer that question. What you can see on the screen here is what we call a Debt-to-Income Calculation for our hypothetical couple; Mary and Joe. The Debt-to-Income Calculation, also referred to as Debt-to-Income Ratio, is a calculation that we make for all loan applications that come through the pre-approval process. What this calculation measures is cash flow on a monthly basis.

In the denominator I’ve listed Mary has a base salary of $5,000 per month gross, or $60,000 per year. Joe as well also has a job that pays him $5,000 a month gross, equaling $60,000 per year. Combined, they make $120,000 per year, which equates to $10,000 per month in qualifying income.

In the numerator, we list their existing obligations. You can see here that Mary has a student loan with monthly payments of $350. Joe has an auto loan with monthly payments of $350. Then there’s some credit card debt here with a small balance and payments of right around $100 per month. In terms of their existing obligations, they pay about $800 per month in existing payments.

In terms of measuring that cash flow, from an approval standpoint most banks are going to allow for 50% of the applicant’s qualifying income, less their existing obligations, to go towards a mortgage payment. So what this calculation does for us over here is calculates that their maximum monthly PITI or mortgage payment would be $4,199.

I think we can all agree here that that level of payment for a couple making $120,000 per year is probably a little bit too expensive. It’s not a prudent decision, it wouldn’t allow them to accomplish other financial goals. In the financial planning community, we typically like to see a couple spending no more than 28% of their gross income on a housing payment. Simple calculation, that works out to be $2,800 per month. In terms of what we call a back end ratio, which takes into account the monthly mortgage payment and their existing obligations, we like to see no more than 36%.

Now in this example, it’s the same number. In other words, 36% of their income less the existing obligations, leaves $2,800 per mortgage payment.

From a financial planning perspective, we would like to see this couple keep their payments at $2,800 or less, the idea being that roughly one third is allocated to housing, a third goes to taxes, and a third can go to savings, consumption, and other needs.

Hopefully that helps you understand your situation. Feel free to email or contact me. Let me be a resource for you. Have a great day.

After two days of the government being shutdown it looks like congress has reached an agreement to fund Federal operations. Just wondering, if this happens again can we ask Canada to govern us?

According to estimates a government shutdown costs the US economy $1 billion per day. Bad news for the economy is often good news for mortgage rates.

Home loan rates need the help because last week they continued to march higher. Interest rates in the US are currently at the highest level since July of 2014. Let’s not lose perspective though, mortgage rates are still historically low.

This week’s economic calendar is relatively light (aside from the government shutdown). On Wednesday we get existing home sales and the FHFA house price index. I expect the latter to reflect continued appreciation due to lack of supply. On Thursday we get the latest reading on new home sales and on Friday durable goods orders.

Assuming that the government funding agreement comes together today I am going to maintain a locking bias. Momentum is not on our side.

If not the uncertainty of the shutdown could help mortgage rates improve in the near-term.

Hi, I’m Evan Swanson with Swanson Home Loans & Mortgage Trust, NMLS number 120856. In this video, I’m going to answer a question that I am frequently asked by home buyers, which is can I build my closing costs into my loan amount in order to reduce my cash out of pocket? I’m going to answer this question today from a purchase transaction perspective. I am not going to address the question from a refinance perspective.

The short answer to the question is no. A home buyer typically is not able to add the closing cost into the loan amount. The reason for that has to do with the loan-to-value restrictions of a loan program.

Let’s look at this with an example. Let’s assume there’s a home buyer who’s purchasing a property for $300,000, and the loan program they’re using requires a 5% down payment. That means they would put $15,000 down and take out a loan for $285,000. Let’s assume, for example, the total closing costs, prepaid, and pro-rated payments for that purchase is $7,000. So, without anything happening, purchase price $300,000, 5% down ($15,000) plus $7,000 settlement charges.

The buyer would have to bring in $22,000 to close. If we were to arbitrarily add that $7,000 into the loan amount, that would push the loan up to $292,000, and now the loan-to-value would be 97%. If the loan program doesn’t allow for a loan-to-value of 97%, then unfortunately the buyer is not able to qualify after adding that in.

There is a backdoor way that we can address this. The buyer could make an offer to the seller for $307,000, but at closing I want you to subsequently give me a $7,000 credit back to be applied to my closing costs.” In that instance, the buyer would have to bring in 5% down based on a $307,000 purchase price, which is $15,350, and now the seller is giving a credit to be applied to the closing cost.

So, the buyer is now effectively able to finance their closing cost by buying the property for a higher price and subsequently asking the seller to give a credit. There are some potential issues around that. In some markets, that may not be viable. In addition, the house would have to appraise for $307,000 to collateralize or to cover that additional $7,000 credit being asked for.

Again, can loan closing cost be built into the loan amount? By default, no, in a purchase transaction. In some instances, you may be able to by effectively building them into your purchase price and subsequently asking the seller to pay them.

Government expeditions aren’t the only thing that have become more expensive. Just take a look at the stock market. Earlier today the Dow Jones Industrial Average (DJIA) eclipsed 26,000 for the first time.

Only seven trading sessions have passed from when the DJIA eclipsed 25,0000. Should it close above 26,000 later today it would be the first time in the market’s 120-year history that it has increased by 1,000 points this quickly.

Momentum in the stock market suggests that home loan rates will have a difficult time moving lower in the near-term. I think the best we can hope for this week is for them to remain constant and I won’t be surprised to see them edge higher.

In my personal opinion US stocks are currently overvalued as compared to long-run valuation comparisons (see HERE) but that doesn’t mean we’ll see a near-term correction.

I warned in yesterday’s post (see HERE) that, “if the yield on the US 10-year treasury note breaks through 2.50% then watch out. I would expect mortgage rates to worsen by another .125%-.25%.”

This morning yields have broken above 2.50% which is not a favorable sign for home loan rates.

There are a variety of factors contributing to the move higher in rates including an expectation for less monetary stimulus in Japan and Europe, growing inflationary pressure, and economic optimism.

It is possible that yields reverse and move back below 2.50% but if that does not happen today and the market closes above this threshold then it will be more difficult for that take place in the near-term.

At this point I would recommend loan applicants lock their rates (if they are able) if they haven’t already.

On this day in 1947 a mother walked into a hardware store in Tupelo, Mississippi and purchased a guitar for her 11-year old son’s birthday. It was his first guitar and the $6.95 investment turned out to be a pretty good one.

In 2004, the son’s estate sold for ~$100 million which equates to a 33.5% annualized return. The power of compound interest brought to you by Elvis Presley.

Mortgage banks only wish they could earn a return of 33.5% on their loans. Rates did tick up last week (modestly) but at today’s 30-year fixed rates it would take 401 years for a $6.95 investment to turn into $100 million. Who’s got time for that?

This week’s economic calendar is relatively light. The highlights include a 10-year treasury note auction on Wednesday, jobless claims on Thursday, and the Consumer Price Index (CPI) on Friday.

From a technical perspective I am keeping a close eye on the US 10-year treasury note (which home loan rates tend to track). It is currently yielding 2.48%. It has not traded above 2.50% in nearly a year. Recent attempts to break through 2.50% have resulted in lower interest rates.

If the yield on the US 10-year treasury note breaks through 2.50% then watch out. I would expect mortgage rates to worsen by another .125%-.25%.

However, if they can hit 2.50% and bounce lower then we may see mortgage rates improve by .125% or better.

Current Outlook: floating as long as the US 10-year treasury note yields less than 2.50%.