Happy New Year! Welcome to 2018. Want to feel old? Students in the class of 2018 that graduate from high school this year were born in 2000-2001. They’ve never known Star Wars to be a trilogy or “rolled down a window”.

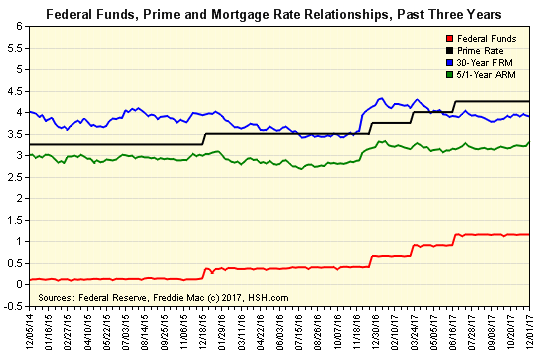

Assuming home ownership rates remain similar then approximately 63% of them will purchase a home in the future. What interest rates will they lock on their loans? If you believe in “reversion to the mean” then this chart above may offer a clue.

I believe mortgage rates are likely to increase in 2018. Why do I think this?

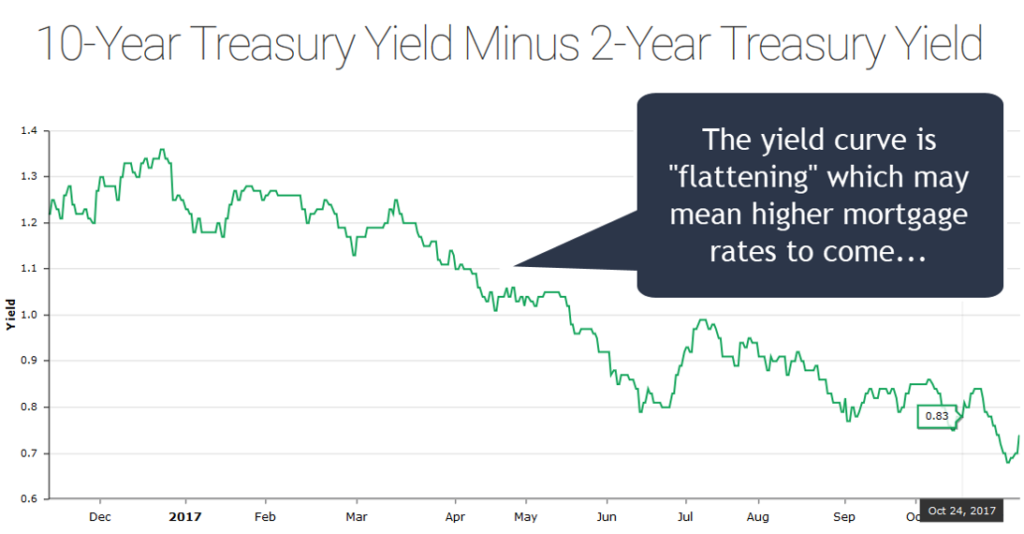

Yield Curve

The yield curve flattened during 2017 as the Fed hiked short-term interest rates while yields at the long end of the curve remain more or less unchanged.

This is evident in the fact that the difference between the yield on a US 10-year treasury note and 2-year note fell last year. A flat yield curve typically predicts an economic recession, which does not seem likely in the near-term, or higher long-term rates in the future. I think the latter is more likely.

I do not have a crystal ball but am forecasting 30-year fixed rate mortgage rates to increase by .50%-.75% during 2018.

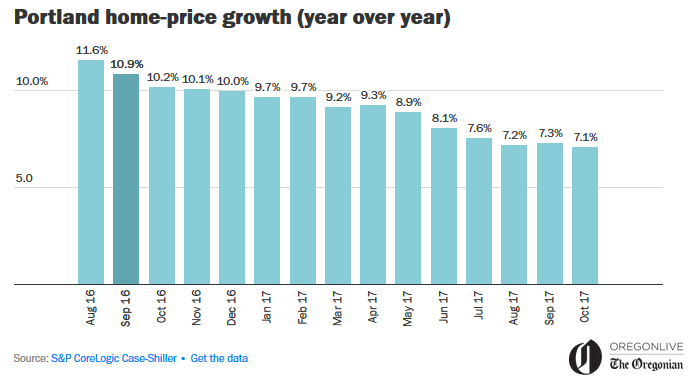

Home Prices

Home price appreciation for Portland has been on a steady decline since the summer of 2016 but remains above historical averages. In Portland home prices are increasing at a ~7% annualized rate according to the Case-Shiller Home Price Index report.

Given that demand is expected to remain strong as people continue to move here and supply of housing remains constrained I think it will be more of the same in 2018. I am forecasting home prices in Portland to increase by 6.0% over the next 12 months.

How do you see 2018 playing out? Feel free to leave comments here.

Current Outlook: locking