If you’re like me then your NCAA men’s basketball bracket is officially busted. With two #1 seeds eliminated in the first weekend I will now focus my sporting attention on the upcoming Masters golf tournament. Speaking of golf, do you know why Virginia and Xavier fans only plan 14 holes? They can’t make it to the final four.

US stocks slide

US stocks fell by approximately 1% last week and are down sharply again today on news that data from Facebook may have been breached in 2016 and improperly used by a third party vendor in the presidential election. Facebook shares are bringing down the broader market.

When stocks decline it typically helps interest rates improve. Thus far mortgage rates are basically unchanged.

The Fed

The Federal Reserve Open Market Committee is scheduled to meet Tuesday-Wednesday with a monetary policy statement slated for Wednesday. The markets fully expect the Fed to hike short-term interest rates by .25%. This is already baked into the mortgage rate offerings you see today.

What can cause interest rates to move are the comments that accompany the rate hike announcement. Will the Fed move more aggressively to hike rates in lieu of recent fiscal stimulus? Or given that recent inflation and wage growth data has been tepid will they stay the course with a “gradual” approach?

Don’t be alarmed when you hear Wednesday afternoon that the Fed is hiking rates by +.25%. It does not necessarily mean that mortgage rates will follow suit.

The rest of the week

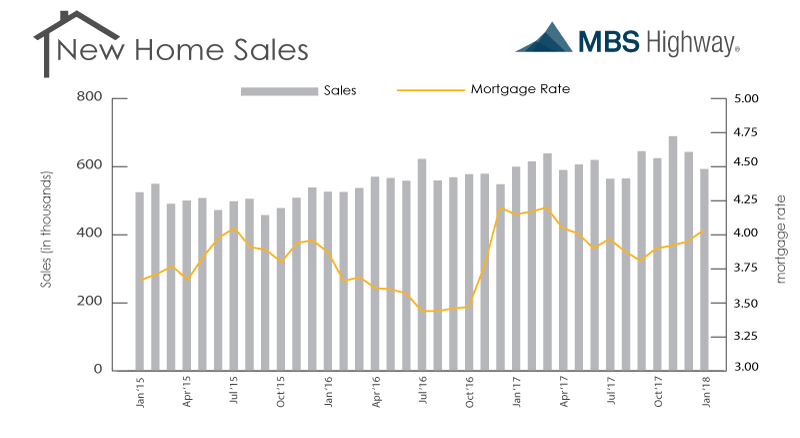

Aside from the highly anticipated Fed meeting I will be watching for the FHFA home price index report due out on Thursday and durable goods along with new home sales on Friday.

From a technical standpoint the yield on the US 10-year treasury note remains below 2.91%. As long as this is the case rates should remain near current levels.

Current Outlook: floating