Mortgage rates are unchanged from last week but accompanying closing costs are modestly lower.

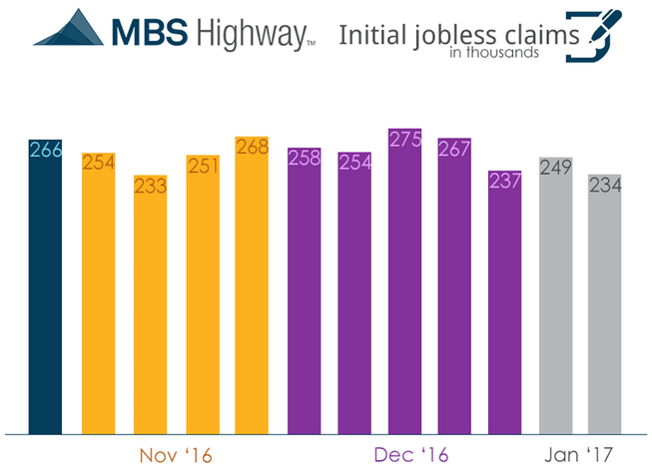

In case you missed it Friday’s all-important jobs report showed stronger than expected hiring (+227,000 jobs) which would normally be a bad signal for mortgage rates. However, average hourly earnings increased by less than expected which tempered inflationary fears. Therefore, mortgage rates had a muted response.

This week’s economic calendar is relatively light. The highlights will come on Friday with import/ export prices and consumer sentiment.

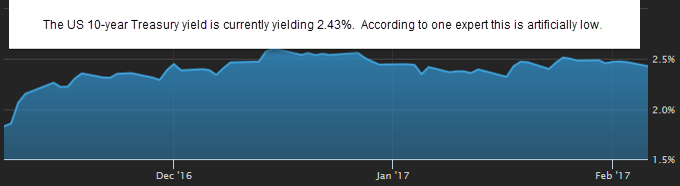

The US 10-year treasury note, which mortgage rates tend to follow, is currently yielding ~2.43%. According to a prominent bond money manager this is artificially low and the markets should expect higher yields in the future. Since the Bank of Japan and European Central Bank are still enacting quantitative easing measures it is placing artificial barriers that are preventing higher rates. Once those programs stall rates will rise. When will that happen? That is up for debate.

Last week President Trump signed an executive order which requires that the Treasury Department take a detailed look at the Dodd-Frank financial regulation law and make recommendations for revisions. It is generally assumed that the president will push to roll back regulations that affect the mortgage industry. It is not clear which rules he is targeting and the Senate will have to approve the changes with a 60 vote super majority (Republicans only hold 52 seats). This is a topic I will be keeping an eye on.

Current Outlook: locking bias