In this week’s edition (see HERE) I include a piece on the pursuit of fulfillment (instead of happiness), an update on reverse mortgages (mortgage insurance premiums will be increasing!), and an article that looks at the CFPB investogation of Zillow advertising.

Category: General Mortgage Info.

Mortgage Rate Update September 5, 2017

According to the calendar summer has passed. From a meteorological perspective autumn began on September 1st in the Northern Hemisphere. However, judging from the temperatures outside it feels like summer remains here in Portland.

What also remains are low interest rates. Mortgage rates improved modestly last week and are firmly at 2017 lows.

As I wrote about last Monday (HERE) the US 10-year treasury note has successfully closed below the important technical level of 2.18% (currently at 2.08%). The last time interest rates were this attractive was during the days following the election in November 2016.

Last week two economic reports in particular helped mortgage rates improve. First, lower than expected inflation data from the Commerce Department called into question the Fed’s plans for continued tightening. According to CME Group there is only a 36% probability that the Fed will hike short-term interest rates again this year. Previously the probability had been greater than 50%.

Second, Friday’s all-important jobs report showed weaker than expected job creation for the month of August. Bad news for the economy is often good news for mortgage rates.

Also contributing to low interest rates is a “flight to safety” in the financial markets. Investors are reacting to news out of North Korea that a nuclear firearm was successfully tested over the weekend and that further tests are planned for the coming days. Anytime geopolitical tension rises interest rates tend to improve.

This week’s economic calendar is relatively light. I expect sentiment regarding the North Korean missile situation will drive action in the financial markets. If tension wanes we could see interest rates worsen and vice versa.

Current Outlook: floating

Reverse Mortgages as a Retirement Tool

It is no secret that the baby boomer generation is entering retirement with troubling financial circumstances. On average baby boomers are carrying more debt, less savings, and fewer guaranteed retirement pensions than previous generations. Need proof? SEE HERE or HERE.

The Home Equity Conversion Mortgage (HECM), also known as a ‘reverse mortgage’, may offer a solution for those retirees who have not accumulated enough retirement savings but have substantial equity in their homes.

The Journal of Financial Planning has done a great job of devoting space to research around the topic of using reverse mortgages as a retirement tool. In the February 2017 issue THIS ARTICLE was featured in which the author compares the usage of a reverse mortgage to an immediate annuity as a funding vehicle.

For those interested in learning more about the basics of a reverse mortgage the author does a nice job summarizing key points in the section entitled ‘The HECM Product’.

In addition, through analysis the author finds that reverse mortgages can generate higher levels of retirement income for couples when compared to the income generated from an immediate annuity. The opposite is true for individuals.

I hope you find it an interesting read! Please feel free to contact me if you want to learn how a reverse mortgage can fit into your retirement plans.

Understanding Tax Deductions on a Residence

I am often asked by customers to explain the tax deductions associated with owning a home. Although I am a CERTIFIED FINANCIAL PLANNER™ I always feel hesitant to answer this inquiry because I am not a licensed tax preparer and the tax code is so dynamic I want to be careful not to misjudge a person’s circumstances.

I came across THIS ARTICLE written by two competent tax professionals and thought I would share it. It does a great job of summarizing the tax advantages of owning a primary & second residence as well as the capital gains exclusion.

The article also touches on the possible advantage of unmarried couples co-owning property in high cost housing areas.

Mortgage Rate Update August 28, 2017

Housekeeping: ‘Rate update’ will be taking a break from laboring one week from today. In honor of Labor Day here is a quote from Robert Orben: “every day I get up and look through the Forbes list of the richest people in America. If I’m not there, I go to work.”

My thoughts and prayers go out to all those affected by the devastating impact of Hurricane Harvey. I wish those who lie in the storm’s wake a safe next few days and rapid recovery.

This week appears to be a pivotal one in terms of the direction of mortgage rates. Since the beginning of July interest rates have improved and mortgage rates are currently at the best levels of the year.

However, the yield on the US 10-year treasury note has idled at the 2.18% level over the past week. Given the amount of significant economic data due out this week I think interest rates will make a decisive move higher or lower in the coming days.

On Tuesday we’ll get the latest reading of the Case Shiller Home Price Index report. On Thursday we’ll get a reading on personal income and pending home sales. Finally, on Friday we’ll get the all-important jobs report, manufacturing activity, and consumer sentiment.

For now I will maintain a floating position but have grown concerned that this trend lower has run out of steam.

Current Outlook: floating

A few ideas worth sharing for August 24, 2017

In this week’s newsletter (see HERE) I include a video which explains why traditional appraisals might be a thing of the past. Also, did you know mortgage rates are currently at 2017 lows? Finally if you like Italian food & wine I provide a link to this weekend’s Italian festival in downtown Portland. Enjoy your weekend!

Mortgage Rate Update August 21, 2017

In case you forgot to “planet” and missed the solar eclipse you can view live feeds HERE, HERE, and HERE.

As the path of the eclipse trends east and south across the United States interest rates are following a similar path. Below is a graph of the yield on the US 10-year treasury note dating back to the beginning of July.

Over that time the yield on the US 10-year treasury note has improved by ~.20% while mortgage rates have improved by .125%-.25%. I don’t expect this trend to last forever but momentum remains favorable for now.

Should the yield break below and close under 2.18% that would be a very good sign for rates to improve further. However, if 2.18% holds then I think we’ll need to shift to a locking bias.

The economic calendar for this week is relatively light until you get to Thursday-Friday. The Federal Reserve Bank will host its annual symposium of central bankers in Jackson Hole, Wyoming starting this Thursday. Both Janet Yellen and European Central Bank President Mario Draghi are scheduled to speak.

Investors are listening for clues as to when the US central bank will begin to unwind its balance sheet and when the European Central Bank will end its version of quantitative easing for the European economy.

I will maintain a floating bias until technical trading patterns shift course.

Current Outlook: floating

Mortgage Rate Update May 15, 2017

On this day in 1800 President John Adams ordered the Federal Government to pack up and leave Philadelphia and move operations to its new home in Washington DC. At the time the Federal Government had 125 employees and the transition took one month. Two hundred and seventeen years later there are now more people employed by the government than in the manufacturing sector.

Speaking of politics I never thought happenings within the FBI would impact mortgage rates. Last week’s controversial firing of James Comey may be helping US interest rates improve. Why? The politically unpopular firing of the former FBI director may encourage those in congress to oppose the President’s proposals on tax reform and infrastructure spending which were generally deemed to be favorable for the stock market and therefore unfavorable for interest rates.

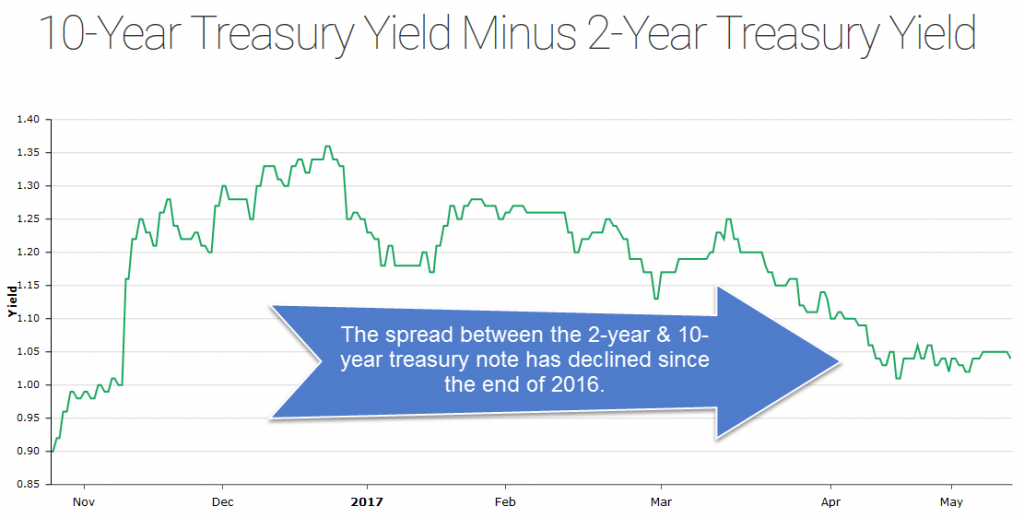

The US yield curve is flattening. The spread between the yield on the US 2-year & 10-year note is now at the lowest level since the election.

This is a signal that the financial markets are less optimistic about the long-term outlook for economic growth. This is also a result of the fact that the Fed continues on a path to hike short-term interest rates. The Fed next meets on June 13th-14th.

From a technical perspective interest rates are in a favorable range. Momentum is on our side but oil prices are moving higher this morning so we’ll want to keep an eye on that market (energy prices are highly correlated to inflation).

Current Outlook: neutral

A Few Ideas Worth Sharing for May 11, 2017

I just published my monthly newsletter with a few ideas worth sharing. In this edition I included an article which explains how two major economic forces could collide and cause mortgage rates to increase later on in 2017, how technology is reshaping the way we live in our homes, and how to reduce stress and live life with greater purpose with a two minute daily habit.

You can check it out and subscribe to my newsletter HERE.

Mortgage Rate Update May 8, 2017

Last week we switched to a locking bias and indeed mortgage rates did worsen very modestly. Rates were pressured higher on Wednesday last week after the Fed labeled weak 1st quarter economic activity as “transitory”.

Friday’s all-important jobs report showed that 194,000 new jobs were created during April and the US unemployment rate fell to a decade low of 4.4%. Good news for the economy tends to be bad news for mortgage rates.

As you’ve probably heard France elected 38 year old Emmanuel Macron to be their new president yesterday. He defeated far right candidate Marine Le Pen. The financial markets are shrugging their shoulders today as it was widely expected.

The Wall Street Journal ran THIS PIECE over the weekend in which they highlight the fact that interest rates are vulnerable to a sharp increase if the Trump administration tax cut plan converges with the Fed’s unwinding of their balance sheet. Should President Trump get his tax cut plan through congress the federal deficit would likely grow beyond the current forecast of $1 trillion by 2023. This coupled with the Fed increasing the supply of bonds on the open market would almost surely drive long-term yields higher. This is a threat we will have to monitor throughout the summer.

In the meantime mortgage rates remain at very attractive levels. This week’s economic calendar is fairly light. The highlights come on Thursday & Friday when we get the Producer Price Index and Consumer Price Index.

The technical outlook for interest rates looks favorable so I am going to recommend a floating bias this week.

Current Outlook: locking bias