Happy May Day! A short history lesson: The earliest accounts of May Day celebrations, meant to celebrate the birth of Spring, dates back the Roman Republic era. However, in the late 19th century Socialist & Communist groups adopted May 1st to be International Workers’ Day in honor of lives that were lost during an attack on striking workers.

Speaking of working this is the first week of a new month and therefore we have the all-important jobs report due out Friday. In fact, the economic calendar is packed with significant events this week.

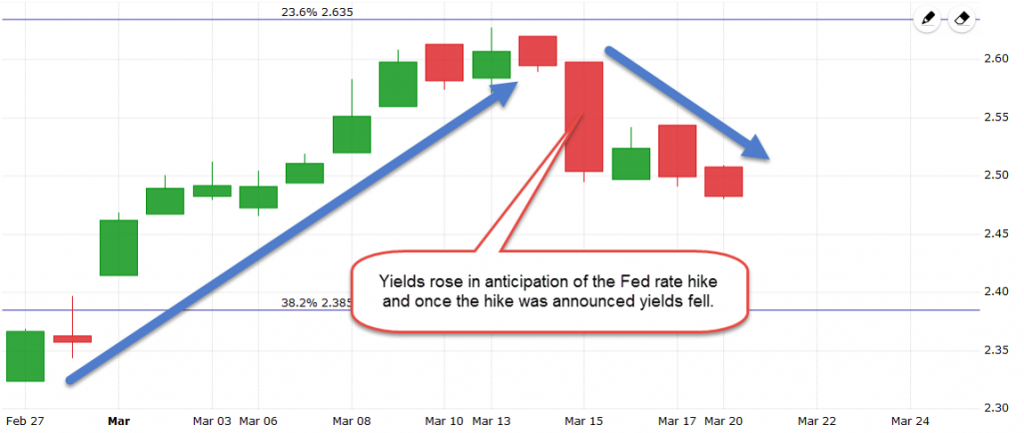

Starting tomorrow the Fed will conduct their regularly scheduled two-day monetary policy meeting. According to CME group there is only a ~5% chance that the Fed will hike short-term interest rates at this meeting. However, the markets think there is a 63% chance they will hike at the next meeting scheduled for June 13th-14th. The Fed does not directly control mortgage rates but their comments and actions can influence them. On Friday five Fed members are scheduled to speak and we’ll get the results of the aforementioned jobs report. I expect to see volatility at the end of the week.

From a technical perspective we are keeping a watchful eye on the yield of the US 10-year treasury note. This morning it broke above 2.31% which was a solid level of resistance.

Should the yield on the US 10-year treasury note close above 2.31% tonight then I think it is likely it will increase all the way to ~2.39% and mortgage rates will likely increase by .125%. For this reason I am going to recommend a locking bias.

Current Outlook: locking bias