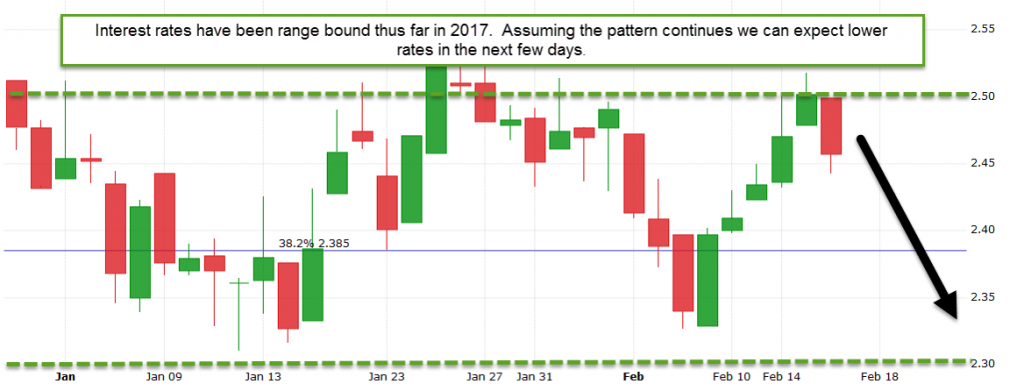

Shifting to a ‘floating bias’ on Thursday of last week has proved timely as yields have improved. Speaking of floating today is National Polar Bear Day. Apparently you can bake “cubcakes” if you really want celebrate.

Mortgage rates had a great ride last week but momentum appears to be shifting. As the French presidential election draws nearer (scheduled to complete May 7, 2017) I expect that polling will be more and more significant for US interest rates. Why?

Anti-European Union candidate Marine Le Pen is considered to be an anti-status quo candidate. The financial markets like certainty. Therefore, when Le Pen’s polling appears stronger US mortgage rates will improve on perceived uncertainty and vice versa. Polling released over the weekend showed her down which is bad news for mortgage rates.

President Trump is scheduled to speak in front of a joint session of congress tomorrow afternoon. Analysts are expecting that he will roll out a major policy initiative. Depending on what that policy is it could impact mortgage rates. Specifically, if he announces a major infrastructure package I would expect mortgage rates to worsen in reaction.

This week’s economic calendar is fairly busy with highlights on Tuesday (GPD) and Wednesday (Personal income & inflation). Given that the technical trading picture has shifted I am going to recommend locking in now.

Current Outlook: locking