Mortgage rates remain at improved levels following last Wednesday’s Fed statement.

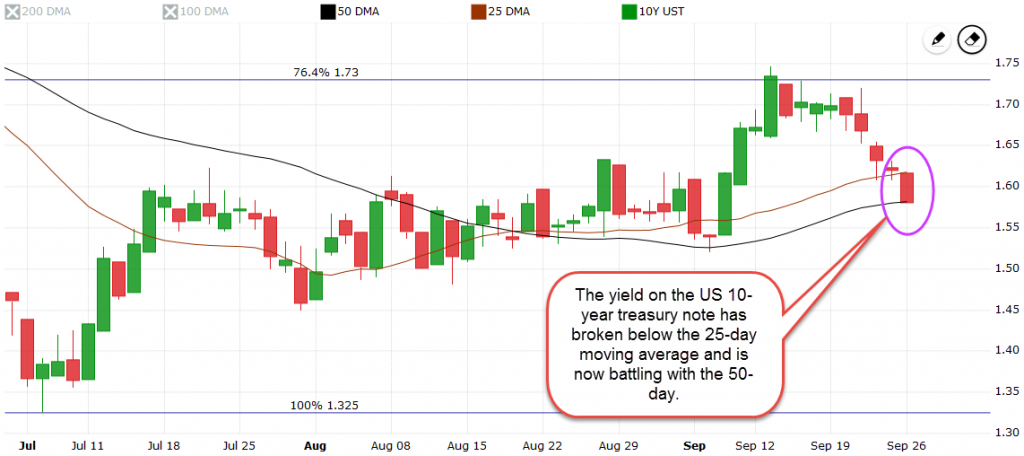

Momentum from the Fed which is favoring mortgage rates may be running out of steam. A quick look at the yield on the US 10-year treasury note, which mortgage rates loosely follow, shows that rates have improved by ~.125%. From a technical perspective the yield has broken below its 25-day moving average (orange line) and is currently trading at the 50-day moving average (black line).

A break below the 50-day moving average could lead to another .125%-.25% improvement in mortgage rates. However, after 5 days of improvement we have to be cautious.

This week’s economic calendar is busy. Earlier today new home sales were reported. New home sales make up ~10% of all home sales. The number of new home sales declined by ~9% from the previous month but that month was a 9-year high.

Later on in the week we’ll get fresh numbers for durable goods orders, gross domestic product, pending home sales, personal income, and the personal consumption expenditure price index. It’s a busy week.

Momentum remains on our side but we need to be cautious give the technical trading patterns (as explained above). The safe money should lock in today.

Current Outlook: cautiously floating