Mortgage rates have increased substantially following the surprise election win by President-elect Donald Trump.

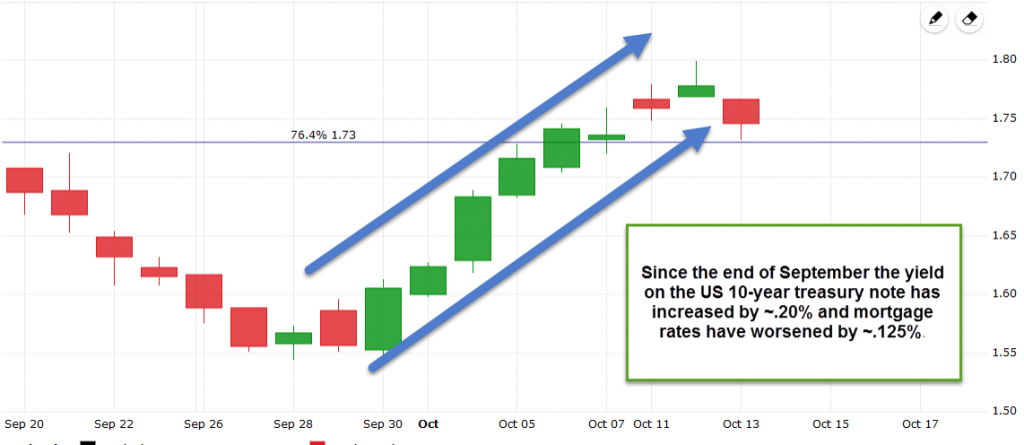

Below is a chart showing the yield on the US 10-year treasury yield. As you can see yields jumped from ~1.80% prior to the election to ~2.20% today. Mortgage rates have increased by .375% during that time.

Why are rates increasing in reaction to Trump’s election? At this point analysts are speculating that his economic policies will be inflationary and inflation is a nemesis for mortgage rates.

Speaking of inflation the economic calendar for this week includes a report on import prices (Tuesday), Producer Price Index (Wednesday), and the Consumer Price Index (Thursday). In addition we’ll get retail sales (Tuesday) and housing starts (Thursday).

From a technical perspective the current outlook is difficult to handicap. On one hand, markets tend to overreact to major events such as last week’s election. Therefore, I wouldn’t be surprised to see rates rebound and improve a little. That said, momentum is firmly against us. So waiting any longer to lock could mean accepting a higher rate than what is available today.

Current Outlook: locking bias