Mortgage rates are slightly improved from Monday.

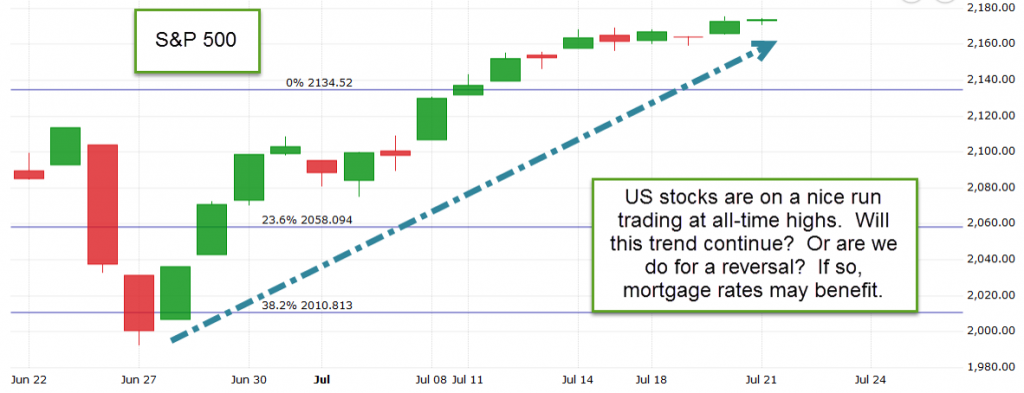

Interest rates here in the US remain near historic lows at the same time as our stock markets hover at all-time highs. I wrote about this unique relationship HERE. Normally when stocks rally it is at the expense of interest rates but given the challenges overseas the US remains a safe-haven.

Consider this, an investor who wishes to have the “safety” of buying bonds (in effect lending the US government money) the current yield on the 10-year treasury note is ~1.54%. Or, they could invest in the 30 stocks in the Dow Jones Industrial Average and earn annual dividends of ~2.78%. Historically bond yields tend to be higher than dividend yields because the equity investor also gets the prospect of stock price appreciation whereas the bond investor is “guaranteed” a return of principal in the future.

The fact that stock dividends are presently higher than bond yields suggests that investors don’t foresee much stock price appreciation in the near-term and/ or believe interest rates will potentially go lower in the future (in which case they could sell their bonds yield 1.54% at a premium).

From a technical perspective US interest rates are treading gingerly at a significant level of support. Should today’s $15 billion US treasury 30-year bond auction be met with weak foreign demand I anticipate mortgage rates could worsen slightly. I recommend locking to play it safe.

Current Outlook: locking bias