Rates are mainly unchanged from Monday. Mortgage rates have improved by .25%-.375% over the past 3 months. The chart below demonstrates the correlation between changes in the US-10 year and mortgage rates.

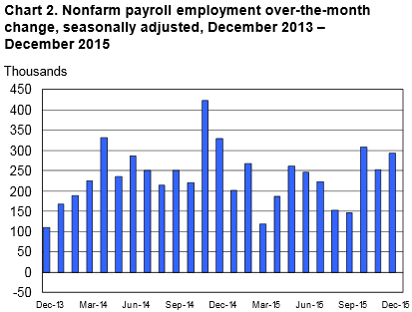

Tomorrow we get the latest all-important monthly jobs report from the Bureau of Labor Statistics. In case you’ve forgotten last month’s report showed that 292,000 new jobs were created but a deeper look into the report showed that many of those were seasonal. As a result, despite the stronger than expected headline number mortgage rates did not increase you we would have expected.

The markets are currently expecting only 188,000 new jobs created during the month of January. Given the lower bar it would seem more likely that the report could surprise to the upside which would hurt mortgage rates. However, looking at the aforementioned chart we do have momentum on our side.

The next Fed meeting is scheduled for March 15th-16th so this jobs report will not have as much significance because there will be one more released on Friday, March 4th.

The monthly jobs report is always difficult to handicap. The momentum in the marketplace is playing to our favor so I am inclined to float. That said, we’ve had a great run in the past 90 days so the safe play is to lock in while we’re ahead.

Current Outlook: locking bias