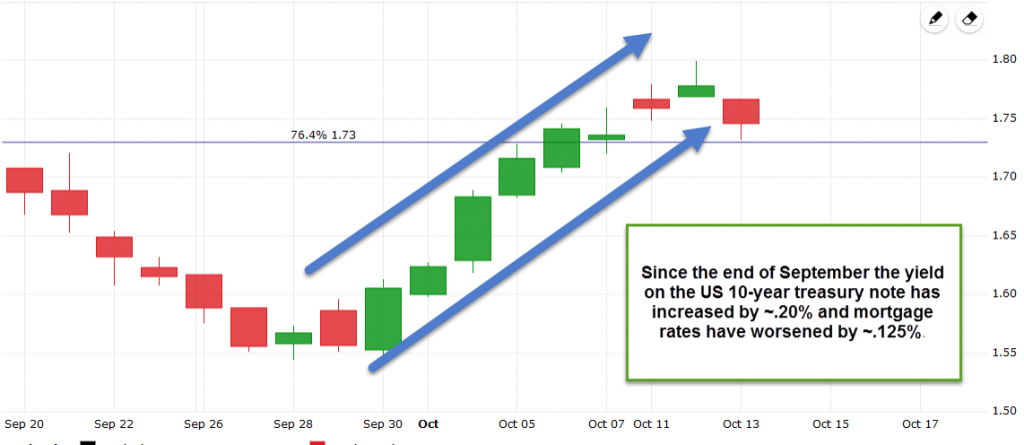

Across the globe long-term interest rates, including those for US mortgages, have worsened this week. A peak at the chart below shows that the yield on the US 10-year treasury note, which mortgage rates tend to track, has risen by ~.50% from the beginning of July until today.

Why the increase?

First, let’s remember that the “Brexit” vote took place at the end of June. Mortgage rates immediately fell sharply as uncertainty spread across the global financial markets and investors sought safe havens for capital.

That uncertainty has dissolved and there is greater confidence in economic growth. As a result, many of the investors who re-positioned investments into the US have reversed those trades which has put upward pressure on interest rates.

Second, inflation expectations are rising across the globe. This is partially related to oil prices increasing. Since February oil prices have risen by nearly 50%. Inflation is the primary driver of long-term interest rates, including mortgages, because it reduces the value of a lender’s future return.

From a technical perspective mortgage rates continue to look vulnerable so I will maintain a locking bias.

Current Outlook: locking bias