On this day in 1961 the Bay of Pigs invasion began. As we know the attempt to overthrow Fidel Castro was a complete failure as it ultimately solidified the relationship between Russia and Cuba and enhanced Cold War tensions.

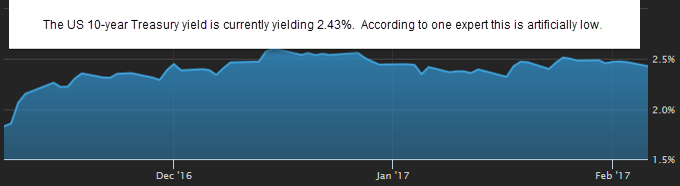

Speaking of tensions US interest rates have benefited from growing geopolitical uncertainty. Global investors do not like being exposed to “risky” assets during potentially turbulent times and therefore we are experiencing a “flight-to-safety” which drives US interest rates down.

Also helping to drive rates lower has been a shift in expectations regarding the Trump Administration’s fiscal stimulus plans. No details have been released but the markets think a much more watered down version will have to be presented in order to win congressional approval. A more aggressive stimulus plan would add inflationary pressure to the economy and hurt interest rates and vice versa.

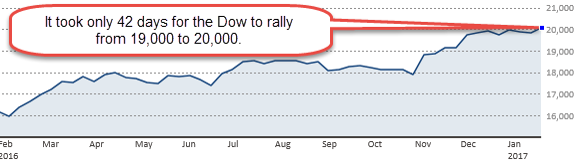

A less aggressive stimulus plan could also hurt US stocks. As measured by the Shiller Price-to-Earnings ratio, which is the ratio of the S&P 500’s price divided by its average inflation-adjusted earnings from the previous 10 years, the stock market appears ripe for reversal. If US stocks do move lower it should help interest rates remain at current levels or maybe even better.

The economic calendar for the week is heavy with fresh housing data. This morning the home builder index, which measures optimism for US home builders, came in slightly below expectations. Tomorrow we get housing starts and building permits. Finally, on Friday the National Association of Realtors will release the latest existing home sales figures.

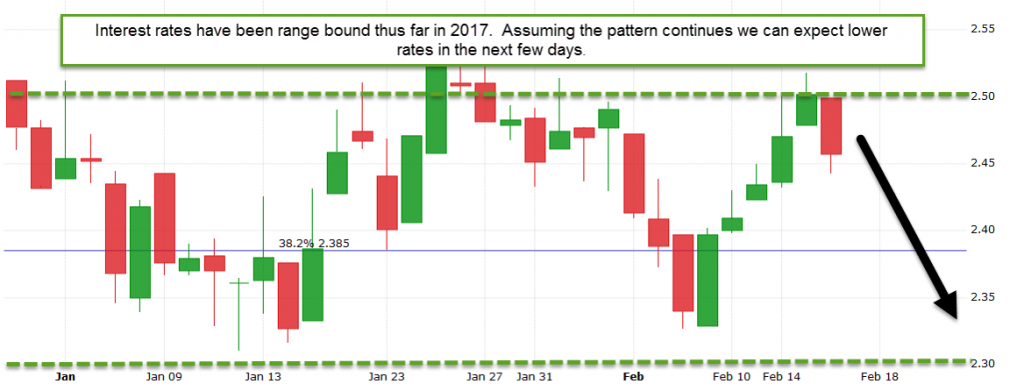

Momentum is still on our side so I will float.

Current Outlook: floating